Sky Harbour (SKYH)

boring private jet leases and boring returns

Sky Harbour (NYSE:SKYH) is developer of private jet hangars with assets in 15 airports. Their business model is simple; buy real estate from airports, build hangars at these airports, and lease them to wealthy private jet owners who need a place to park their jets. SKYH specializes its hangars to serve higher end clients by including amenities in their hangars. Amenities include climate control, private lounges, dedicated line services, and in-hangar maintenance capabilities. Another special thing about SKYH is that they are the first hangar developer (that I know of) to not also run a Fixed Based Operator (FBO) business. Historically most hangar developers also operated FBO’s to provide fueling, towing, de-icing, maintenance, and waste removal services. SKYH has deliberately chosen to focus on providing premium, exclusive-use private hangars for private jets, diverging from the traditional Fixed Base Operator (FBO) model. This means that SKYH does not have to deal with the volatility of energy prices and the capital intensity related to FBOs. Instead, tenants will need to purchase FBO services from another FBO in the airport.

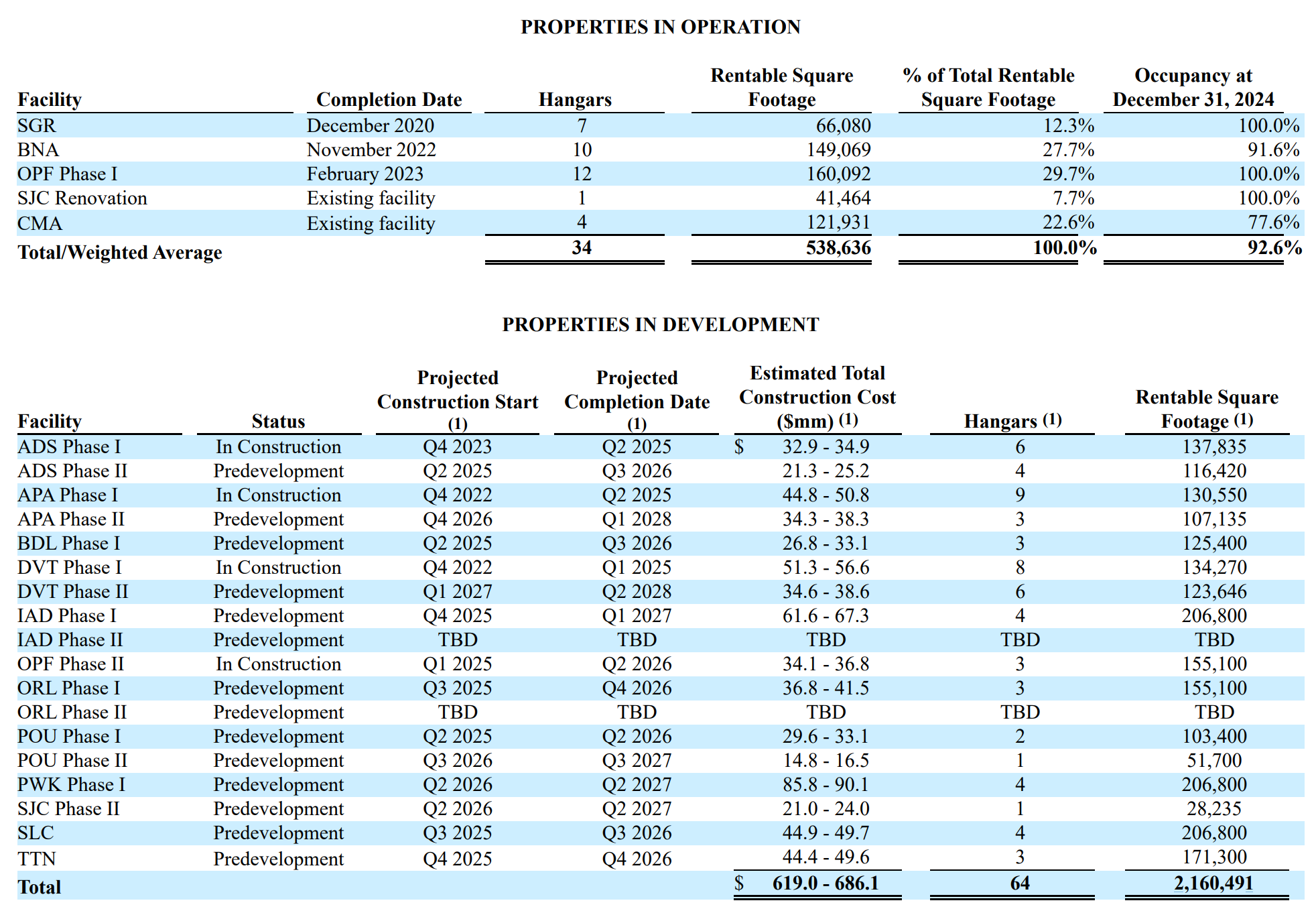

I found this company screening for negative gross margin firms with large debt loads, aka. shitcos. Their shitty financials on the surface do not tell the full story though. Their recent 10-K shows that they own 2.6M in square feet of airport real estate with 538K being operational hangars and leased at a 92.6% occupancy rate.

Lets model this!

Assuming most projects are completed by Q4 2026 as planned, and there are no new acquisitions of airport real estate, lets see what the rental income looks like in 2027 to gauge what forward yield we can get if we buy SKYH today. This is a difficult estimate to make since there are a few uncertainties. Firstly, we have to estimate the annual rent per square foot. As of Q3 2024, management told us it’s currently sitting at $40 per square foot. This is much higher than the anticipated $30 and shows that these specialized hangars have been rewarded a higher premium that originally expected.

We can see lease hangar inflation data to get a rough estimate of what this current $40 rate will look like in 2027, which is 4%. We also have to recognize that this demand is growing and will continue to grow so I will throw on an additional 1% in hangar rate inflation, which I think is fair. This gets a 2027 dollar per square foot of $44.5.

The next uncertain estimate in our model is going to be the occupancy rate, which management says that they can and will continue to be able to operate at a greater than 100% occupancy rate due to multiple tenants at a time. But lets be real, CMA (Camarillo Airport), which they acquired in December 2024 only has a 77.6% occupancy rate, which while new, shows that this exaggerated 100%+ number on the 10-K is going to be extremely unlikely in 2027 and is only a long term goal for the firm. Using my high quality guesstimations, I got a 88.2% average occupancy rate on the 2.3M in completed hangars in 2027.

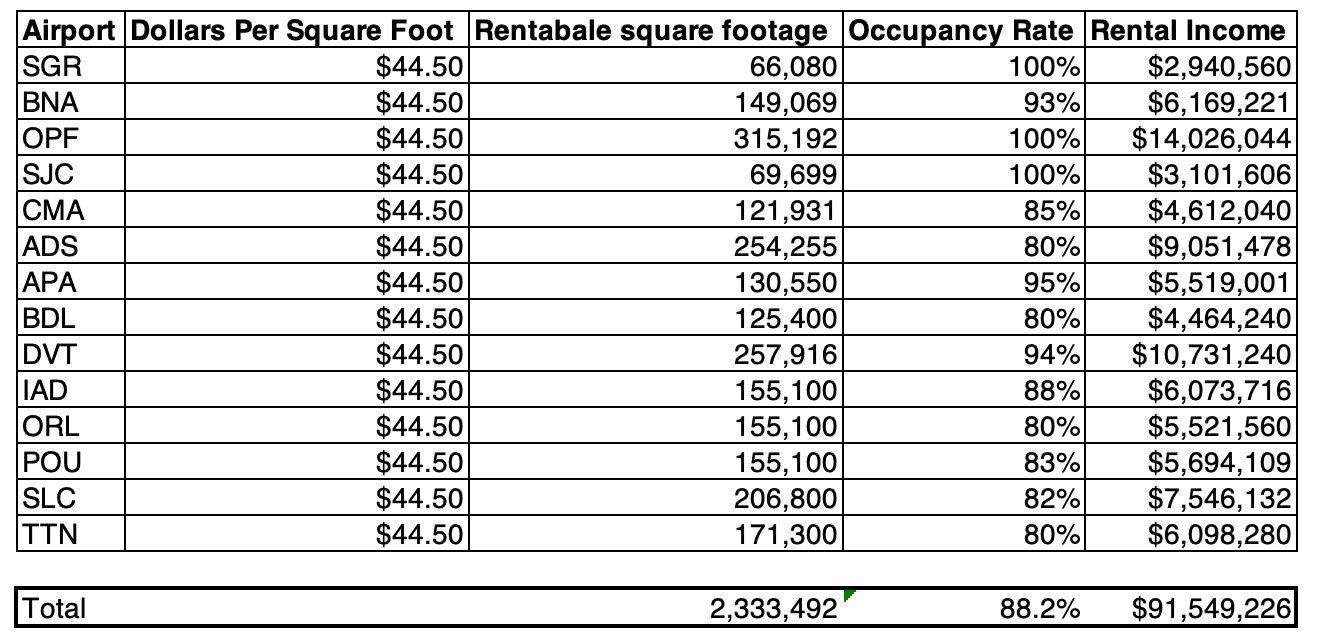

Below we can see my estimates for how much SKYH will recieve in rental income in 2027. I got $91.5M in year end 2027 rental income. This does not include some projects that won’t be finished until late 2027 and early 2028.

To make matters more complicated, SKYH has private placement PIPE warrants (SKYH/W) that expire on January 25, 2027 with a strike price of $11.5 (currently ITM) that will dilute the market cap considerably, by 624M to be exact.

Conclusion

So when its all said and done, SKYH will give you 6.5% yield BEFORE operating expenses, which I haven’t even begun to try and estimate. While this play is exciting, and the private jet market looks promising, I think SKYH is a “wait and see” sort of situation. If the stock sells off considerably, it deserves a revisit. If it continues to go up, you have lost your opportunity. I also want to mention that the IAD hangars, of which only half are TBD, are likely to be a massive market and could change things if any developments come out. Right now, it doesn’t make sense do buy SKYH today, wait through dilution overhang, and only get a 6.5% yield in 2027.

SKYH probably rejects this $14 level as it has many times before. At $8 though, that yield starts to become more attractive and will certainly be revisited by yours truly.

Thank you for your time!

Disclaimer: The information provided in this substack is for general informational purposes only and does not constitute financial, investment, legal, or other professional advice. All opinions expressed are solely those of the author. You should not rely on the information provided as a substitute for professional advice tailored to your individual circumstances. Always consult with a qualified financial advisor or other professional before making any investment or financial decisions. The author assumes no liability for any actions taken based on the information contained in this post.